Money Management Tips for Beginners, Managing your finances effectively is a cornerstone of personal and professional success. For beginners, understanding and applying the basics of money management can set the stage for a secure financial future. This guide will walk you through essential tips and strategies to manage your money wisely.

Understand Your Financial Goals

Before diving into budgets or investments, it’s crucial to establish clear financial goals. Knowing what you’re saving or spending for gives your money a purpose.

Short-term Goals For Money Management:

These include objectives you want to achieve within a year, such as building an emergency fund or saving for a vacation.

Long-term Goals Money Management:

Long-term goals, like buying a house, starting a business, or retiring comfortably, require sustained effort and strategic planning. Write your goals down and assign realistic timelines to each.

Track Your Income and Expenses:

Understanding where your money comes from and where it goes is fundamental.

Tools For Tracking:

- Apps: Apps like Mint, YNAB (You Need a Budget), or PocketGuard can simplify tracking.

- Spreadsheets: A simple Excel or Google Sheet can also do the job.

Categorize Your Expenses

Divide your expenses into essentials (rent, utilities, groceries) and non-essentials (entertainment, dining out). This will help you identify areas where you can cut back.

Create a Budget

A budget is your financial roadmap. It helps you allocate income toward expenses, savings, and investments.

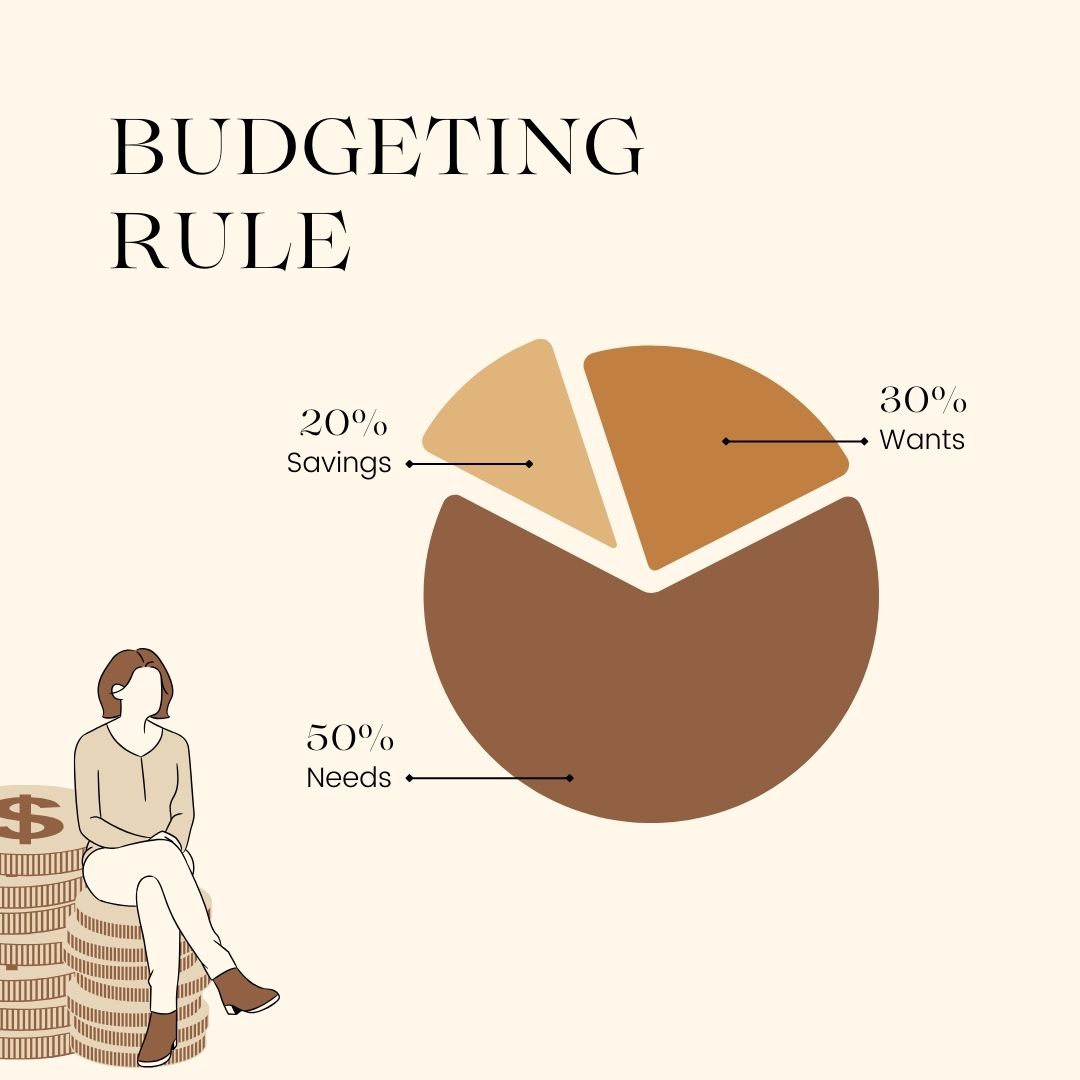

The 50/30/20 Rule for Money Management:

- 50% for necessities like rent, utilities, and groceries.

- 30% for discretionary spending like dining out or hobbies.

- 20% for savings and debt repayment.

Zero-Based Budgeting

This method ensures every dollar has a purpose, whether it’s for bills, savings, or leisure.

Build an Emergency Fund

An emergency fund acts as a financial safety net.

How Much to Save?

Start with a goal of three to six months’ worth of living expenses. This cushion can help you handle unexpected events like medical emergencies or job loss.

Where to Keep It?

Use a high-yield savings account for your emergency fund to ensure easy access and modest interest earnings.

Understand and Manage Debt

Debt can either be a tool or a trap, depending on how it’s managed.

Good Debt vs. Bad Debt

- Good Debt: Mortgages or student loans that contribute to your future.

- Bad Debt: High-interest credit card debt or payday loans.

Strategies for Managing Debt

- Pay more than the minimum payment on your loans.

- Use the Debt Snowball Method (pay off the smallest debt first) or the Debt Avalanche Method (pay off the highest interest debt first).

Start Saving Early:

The earlier you start saving, the more you benefit from compound interest.

The Power of Compound Interest

Compound interest helps your savings grow exponentially over time. For instance, investing $100 per month at a 6% annual return can grow significantly over 20 years.

Automate Your Savings

Set up automatic transfers to your savings account to ensure consistency.

Learn the Basics of Investing

Investing can help you build wealth over the long term

Investment Options for Beginners

- Stocks: Ownership in companies.

- Bonds: Loans to companies or governments.

- Mutual Funds: Pooled funds managed by professionals.

- ETFs (Exchange-Traded Funds): Similar to mutual funds but traded like stocks.

Start Small

Platforms like Robinhood, Acorns, or Vanguard allow beginners to start with minimal amounts.

Live Below Your Means

Avoid lifestyle inflation, where increased income leads to increased spending.

Practical Tips for Money Management:

- Resist the urge to upgrade your lifestyle with every raise.

- Embrace frugal habits like cooking at home, using public transport, or buying second-hand items.

Understand Credit and Build a Good Credit Score

Your credit score affects your ability to borrow and the interest rates you’ll pay.

Tips for Building Credit

- Pay bills on time.

- Keep your credit utilization ratio below 30%.

- Avoid opening too many new accounts in a short period.

Benefits of a Good Credit Score

A high credit score can help you secure loans at favorable terms and lower interest rates.

Educate Yourself Continuously

Financial literacy is an ongoing process.

Resources

- Books: Rich Dad Poor Dad by Robert Kiyosaki, The Total Money Makeover by Dave Ramsey.

- Podcasts: The Dave Ramsey Show, How to Money.

- Courses: Platforms like Coursera and Udemy offer personal finance courses.

Stay Informed

Regularly read financial news to understand economic trends and opportunities.

Avoid Impulse Purchases

Impulse buying can derail your budget.

Strategies to Curb Impulse Spending

- Follow the 24-hour rule: Wait a day before making non-essential purchases.

- Unsubscribe from promotional emails to avoid temptation.

- Create a list before shopping and stick to it.

Protect Your Financial Future

Insurance and retirement planning are crucial for long-term stability.

Insurance

- Health Insurance: Covers medical emergencies.

- Life Insurance: Provides for your dependents in case of unforeseen events.

Retirement Planning:

Start contributing to retirement accounts like a 401(k) or an IRA early. Take advantage of employer matches if available.

Seek Professional Advice When Needed

A financial advisor can provide personalized advice based on your situation.

When to Consult an Advisor

- Planning for retirement.

- Managing significant debt.

- Understanding complex investments.

Look for certified professionals (e.g., CFP or CFA) to ensure credibility.

Review and Adjust Regularly

Financial planning isn’t a one-time activity.

Monthly Reviews

Check your budget and expenses monthly to ensure alignment with your goals.

Annual Reviews

Evaluate your progress toward long-term goals annually. Adjust savings or investment plans as needed.

Mastering money management is not about earning more but managing what you have wisely. By setting clear goals, sticking to a budget, saving diligently, and continuously educating yourself, you can take control of your finances and build a secure future. Remember, small, consistent steps lead to significant results over time. Start today and make financial success your reality!

FAQ: Money Management Tips for Beginners

1. What is money management, and why is it important?

Money management involves budgeting, saving, investing, and spending wisely to achieve financial stability and goals. It’s essential to avoid debt, build wealth, and prepare for unexpected expenses.

2. How do I create a budget?

Follow these steps:

Calculate your total income.

List your monthly expenses (fixed and variable).

Allocate funds using a method like the 50/30/20 rule:

50% for needs (rent, groceries).

30% for wants (entertainment).

20% for savings and debt repayment.

3. How do I stay consistent with money management?

Review your budget regularly.

Automate savings and bill payments.

Set reminders to track expenses and financial goals.

4. When should I start planning for retirement?

The earlier, the better. Take advantage of employer-sponsored retirement plans (e.g., 401(k)) or open an IRA to benefit from compound growth.

5. What are some common money mistakes beginners make?

Living beyond their means.

Not having a budget or emergency fund.

Ignoring debt repayment.

Failing to plan for retirement.

6. How can I start investing as a beginner?

Educate yourself about investment options like stocks, bonds, mutual funds, and ETFs.

Use beginner-friendly platforms like Robinhood, Acorns, or Vanguard.

Start with small amounts and focus on long-term growth.